This affect borrower eligibility can present in mortgage assertion costs, and this enhanced dos percentage factors to 14 percent for all pick borrowers when you look at the 2022. DTI ratio is actually conveyed while the leading reason for assertion.

The speed raise has not yet affected individuals and houses similarly

Breaking the actual reduction in get mortgage loans by the some other borrowing and you will borrower characteristics can show and therefore potential buyers was in fact disproportionately sidelined. Full, the newest offers away from reduced-money and you may higher-combined-loan-to-worth (CLTV) consumers per refused by throughout the twenty-two per cent.

How many mortgages originated so you can white borrowers stopped by the high display, that’s more than likely explained by light house becoming very likely to features an existing financial with an interest price near 3 percent, definition they would have less added bonus to go.

To possess light borrowers which have reasonable profits, the brand new decrease in originations is actually just like the full decrease, but for consumers regarding color, the latest decline is much more pronounced. Financing to individuals with reduced earnings fell 4.5 fee things more than overall credit having Black borrowers, 5.seven percentage things a lot more for Hispanic borrowers, and you can 8.seven fee things far more to own Asian consumers. It testing means that individuals away from colour having lower incomes you will definitely be much more sensitive to rate alter because they do not feel the wide range to put together more substantial deposit so you can mitigate new aftereffects of price grows.

This new show from originations with a high CLTV ratios fell the quintessential to own white individuals. Although significantly more studies are necessary, it will be possible one to an increased show away from light borrowers-exactly who, on average, convey more wealth-were able to go on to less CLTV class which have a beneficial huge deposit, while many Black colored and you will Hispanic properties dropped outside of the homebuying business.

Lastly, the new share of money buyers in addition to show out-of buyers enhanced from the . Considering studies out-of Agent, the fresh express of cash people increased off thirty two.4 per cent in order to thirty-six.1 percent during this time period. The new buyer express, provided with installment loans for bad credit Cleveland CoreLogic, increased of thirty-two.one percent so you’re able to forty.1 percent. These types of alter recommend that the interest rate increase strengthened the newest cousin to get energy of them that have deeper financing, as they possibly can establish a larger down payment or shell out completely during the dollars.

Numerous procedures and software can increase use of homeownership from inside the an excellent high-rate ecosystem

Ascending interest rates features suppressed the amount of mortgages getting originated thanks to worsened affordability, nevertheless the impression is more intense having financing with attributes toward new margins out of qualifications. Consumers who possess less overall to get off and lower income and have a tendency to show the low stop away from homeownership regarding the You.

Price buydowns, hence help borrowers secure straight down rates by paying having points in advance, can offer one to solution to look after accessible homeownership through the higher-speed episodes. Buydowns decrease DTI percentages while increasing the latest much time-title value off home loan loans. Programs that offer speed buydowns because of provides otherwise forgivable funds could possibly get assist consumers you to definitely wouldn’t be in a position to manage home to their own.

To possess borrowers exactly who do not want buydowns, expanding business out of downpayment direction software, in addition to special purpose credit programs (SPCPs), may help. SPCPs are run of the personal lenders to aid historically disadvantaged groups access borrowing. Most SPCPs currently render down-payment and you can closure pricing direction, that may along with assist lower the DTI proportion and up-side costs regarding homebuying.

Versus such procedures or other people that can down traps for consumers having a lot fewer information, the fresh new disproportionate refuse regarding homebuying from inside the higher-rate surroundings you’ll worsen existing homeownership and you can wealth gaps.

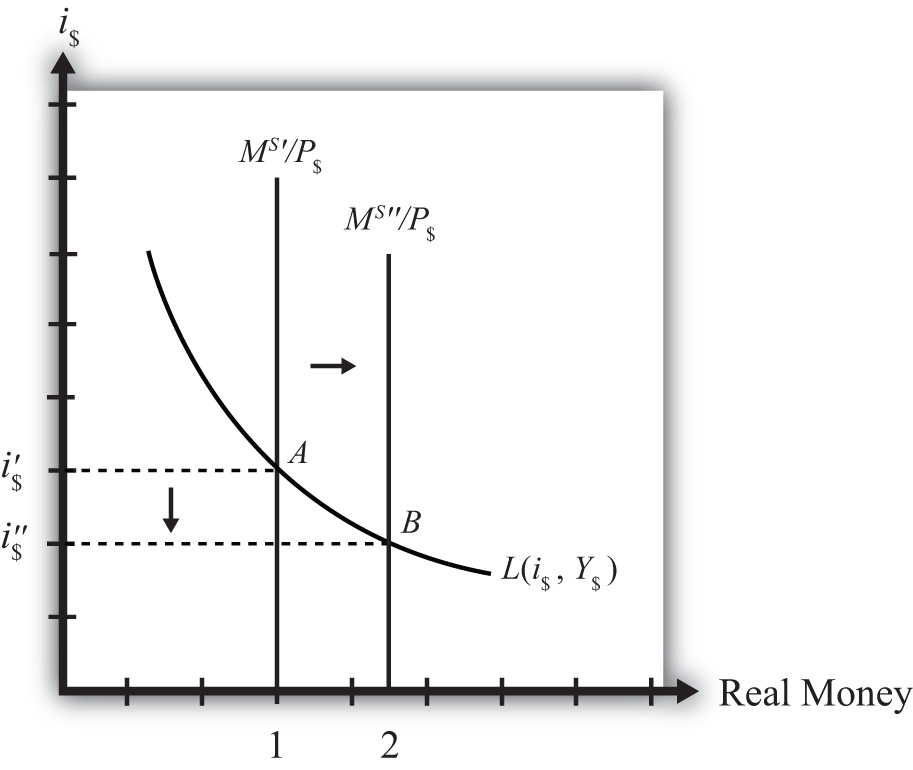

High costs along with apply at home loan borrowing from the bank. As rates rise, thus does good borrower’s financial obligation-to-money (DTI) ratio. Mortgage software possess DTI thresholds that determine qualifications. In the event that a good borrower’s DTI proportion surpasses 50 %, it is difficult to obtain a conventional mortgage, and if an effective borrower’s DTI ratio try more than 57 per cent, the new borrower was ineligible to have Federal Houses Government fund. Of several borrowers that would was according to the DTI endurance into the 2021 have been pushed above they because of the rate increase (PDF).